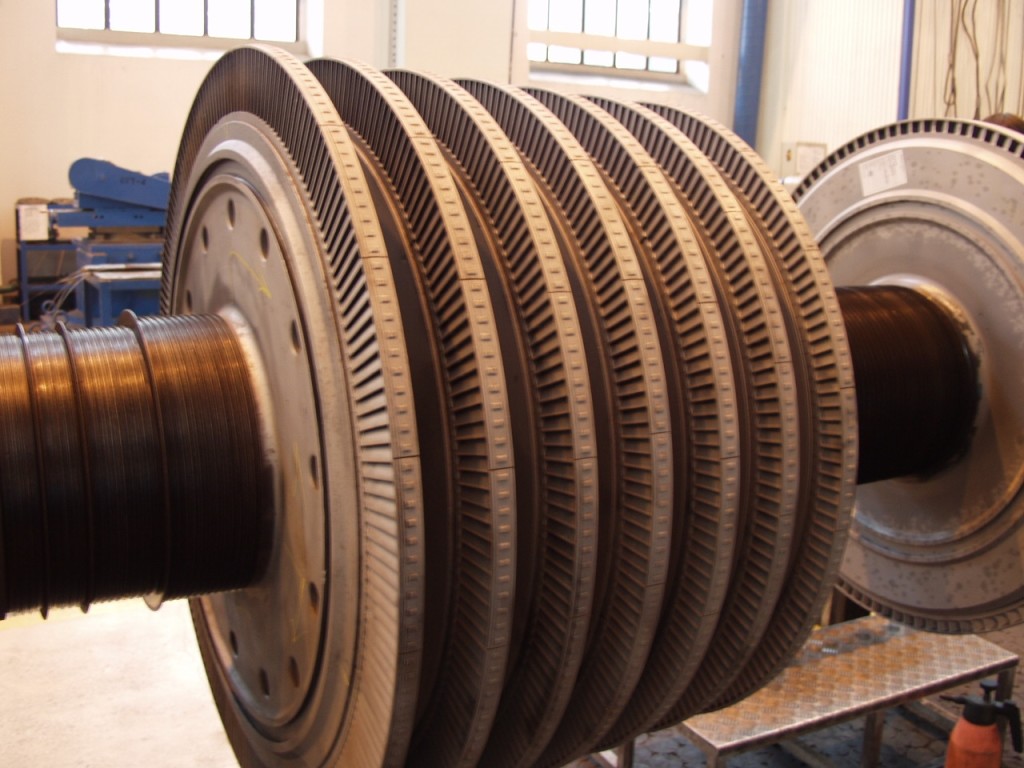

The breakdown was caused by damage of the axial – carrying bearing of the shaft. The damage occurred as a result of excessive (larger than recommended) axial clearance formed by violent destruction in a few minutes of the surface of one of the pressure shoes’ series in the bearing by its wipe. Before the breakdown, the clearance was smaller than recommended. At the same time, just before the breakdown, the enlargement of the turbine load and growth of the steam flow took place, which caused expansion of axial pressure on the bearing liner. In such circumstances of small clearance, it is possible to disturb the lubrication system of the pressure shoes having contact with the axial collar (ring) of the journal. It caused the increase of the shoes’ temperature and transition of the elements’functioning from smooth or semi-smooth friction to dry friction as well as initiating the abrasive destruction of the pressure shoes. As mentioned above, the result was excessive axial clearance that automatically shut off the turbine. It is possible, with regard to the last exploitation period of the turbine, just before a planned repair, the level of discernible wear in the bearing liner was considerable resulting in a lack of axiality in the rotor’s work, including non-perpendicular pressure of pressure shoes on the stopper ring of the shaft. It could have influenced the disturbance in the lubrication process at the moment of turbine load. This could not be confirmed with any certainty.

The breakdown of the turbine set caused signiificant losses associated with repair costs and had a negative influence on the inancial results of claimant. Fortunately, the breakdown in question was covered by a business interruption policy. The loss of profit was caused by the fall of turnover resulting from a breek in power production by the damaged turbine set and by the turbine set in the cascade system. A specific technological system allowed for further production to a limited extent by an undamaged turbine set while reparation of the damaged set was carried out and this diminished the scope of the loss. The claimant overstated the claim value claiming for the value of the loss in turnover without correction and using a coefficient of gross profit.